I've written two articles about Hexza Corporation Bhd: the first one, HEXZA: My Selected Viewpoints Retraced on 09/04/2015 and the second, HEXZA: 2016年最值得期待的十大价值股之一 on 25/01/2016. Some influential authors in i3investors and other places have also written excellent articles, sharing their thoughts on HEXZA. The following links are some well-written articles, which I think are still very readable.

01/12/2015 Insider Asia’s Stock Of The Day: HEXZA (01/12/2015)

23/11/2015 HEXZA - Post Q1 2016 - Gainvestor 10sai

17/11/2015 HEXZA - Chemical Solution - Gainvestor

03/09/2015 [转贴] Hexza Q4'15 成绩单 - 糊涂

27/07/2015 Hexza gains traction

21/07/2015 Hexza - One Hex Higher - Bonescythe Stock Watch | I3investor

15/02/2015 (Icon) Hexza Corp - Manufacturer of Formaldehyde Based Adhesive and Resins

12/02/2015 [转帖] 价值股精选- Hexza - 糊涂- Good Articles to Share |

This article, my third on HEXZA, "What, When, and Why on It and The Answers from A Minority Shareholder," and perhaps the last of my articles on it appeared in i3investor. Why? My reason is at the end of this article.

So, what come first? The fundamentals from publicly available sources...

What the company is doing?

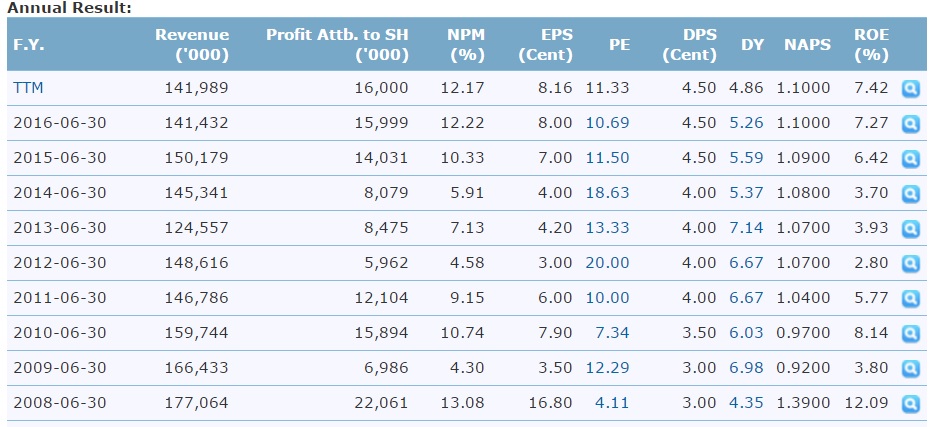

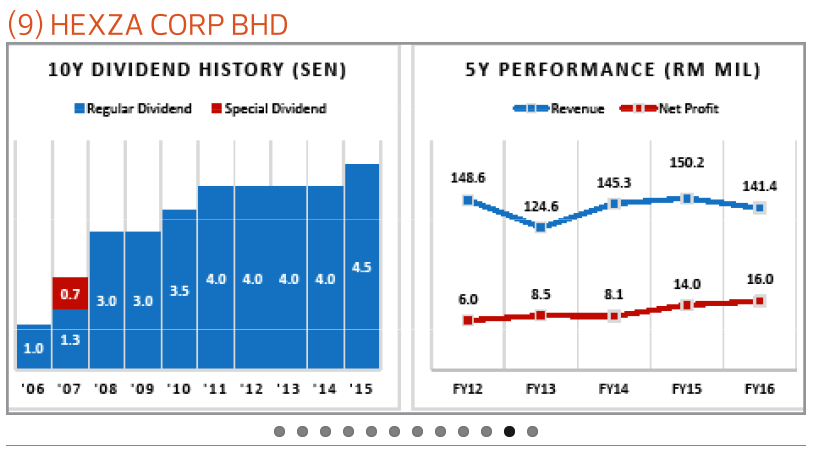

Then, how's the company financial performance in recent years?

And what about its share price?

Latest Financial Results and Prospects

So now, why HEXZA?

And why not others?

The point is: When it’s still undervalued.

Why it's still undervalued? By the way, read the copy and paste from the Star, "In the late 1990s, the stock was among the favourites trading at above RM2.50 before collapsing alongside concerns that valuations of the entire stock market had run ahead of fundamentals." Yes, HEXZA has been undervalued for so many years. An article on HEXZA written in Mandarin gives these reasons: low profile management and under-covered/under- researched by investors, google this if you're interested and know Mandarin [股海宝藏:管理层作风低调投资者未详加研究 喜兹泽仍落后大市 2009/08/04].

The above-mentioned reasons might be well accepted at that time. But a lot of things have changed since then. We've seen that the top management has done some remarkable efforts to improve the company's top- and bottom-line and its financial position, as highlighted above.

As mentioned above, some influential authors in i3investors and other places have also written excellent articles, sharing their thoughts on HEXZA.

So, why it's still undervalued?

The possible explanation could be, as of now, we haven't seen a prominent investor that has accumulated enough shares and the timing for him/her to push the share price up is yet to come.

Why am I saying so? Few years back, I bought some GTRONIC at around 90 cents, PBA at around 90 cents, LCTH at 12-25 cents, Latitude at around 70 cents, just to name a few. And then, when those stocks flying high and skyrocketing, you guess who is in?

Now let's take a look at the shareholders statistics for the past 15 years or so.

No. of shareholders: 16667 (10-04-2001)... 10170 (28-09-2009), 8874 (28-09-2012), 8578 (01-10-21013), 8418 (26-09-2014), 8162 (30-09-2015), *check for 2016* Note: up or down? What does it means and why?

See the latest annual report for the top-30. Who you guess will be the next prominent investor in HEXZA?

What else?

I googled “HEXZA” and “Hexza Corporation BHD, and found the following.

With all the above, what should be the fair price of HEXZA? I think it's worth at least RM1.10 per share, as its NTA and that's above 4% dividend yield, well above the fixed deposit.

Just for sharing.

By Bugle

01/12/2015 Insider Asia’s Stock Of The Day: HEXZA (01/12/2015)

23/11/2015 HEXZA - Post Q1 2016 - Gainvestor 10sai

17/11/2015 HEXZA - Chemical Solution - Gainvestor

03/09/2015 [转贴] Hexza Q4'15 成绩单 - 糊涂

27/07/2015 Hexza gains traction

21/07/2015 Hexza - One Hex Higher - Bonescythe Stock Watch | I3investor

15/02/2015 (Icon) Hexza Corp - Manufacturer of Formaldehyde Based Adhesive and Resins

12/02/2015 [转帖] 价值股精选- Hexza - 糊涂- Good Articles to Share |

This article, my third on HEXZA, "What, When, and Why on It and The Answers from A Minority Shareholder," and perhaps the last of my articles on it appeared in i3investor. Why? My reason is at the end of this article.

So, what come first? The fundamentals from publicly available sources...

What the company is doing?

Then, how's the company financial performance in recent years?

And what about its share price?

Latest Financial Results and Prospects

So now, why HEXZA?

And why not others?

The point is: When it’s still undervalued.

Why it's still undervalued? By the way, read the copy and paste from the Star, "In the late 1990s, the stock was among the favourites trading at above RM2.50 before collapsing alongside concerns that valuations of the entire stock market had run ahead of fundamentals." Yes, HEXZA has been undervalued for so many years. An article on HEXZA written in Mandarin gives these reasons: low profile management and under-covered/under- researched by investors, google this if you're interested and know Mandarin [股海宝藏:管理层作风低调投资者未详加研究 喜兹泽仍落后大市 2009/08/04].

The above-mentioned reasons might be well accepted at that time. But a lot of things have changed since then. We've seen that the top management has done some remarkable efforts to improve the company's top- and bottom-line and its financial position, as highlighted above.

As mentioned above, some influential authors in i3investors and other places have also written excellent articles, sharing their thoughts on HEXZA.

So, why it's still undervalued?

The possible explanation could be, as of now, we haven't seen a prominent investor that has accumulated enough shares and the timing for him/her to push the share price up is yet to come.

Why am I saying so? Few years back, I bought some GTRONIC at around 90 cents, PBA at around 90 cents, LCTH at 12-25 cents, Latitude at around 70 cents, just to name a few. And then, when those stocks flying high and skyrocketing, you guess who is in?

Now let's take a look at the shareholders statistics for the past 15 years or so.

No. of shareholders: 16667 (10-04-2001)... 10170 (28-09-2009), 8874 (28-09-2012), 8578 (01-10-21013), 8418 (26-09-2014), 8162 (30-09-2015), *check for 2016* Note: up or down? What does it means and why?

See the latest annual report for the top-30. Who you guess will be the next prominent investor in HEXZA?

What else?

I googled “HEXZA” and “Hexza Corporation BHD, and found the following.

With all the above, what should be the fair price of HEXZA? I think it's worth at least RM1.10 per share, as its NTA and that's above 4% dividend yield, well above the fixed deposit.

Just for sharing.

By Bugle

No comments:

Post a Comment